Across all industries, the labour landscape remains underwater

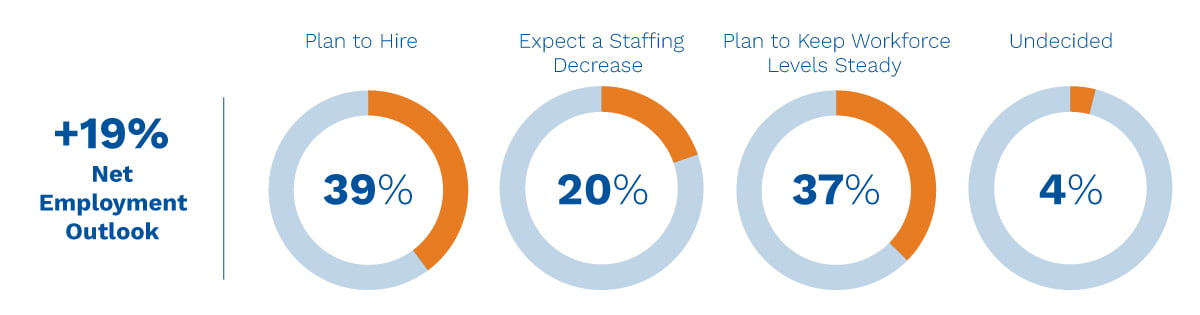

Even though the UK employment outlook has begun to cool, with hiring intentions down 5% from Q4 2022 into Q1 2023, demand for key workers continues to outstrip supply. In almost every industry and across businesses of all shapes and size, almost 50% of organisations state an inability to secure the talent they need is their biggest challenge to growth.

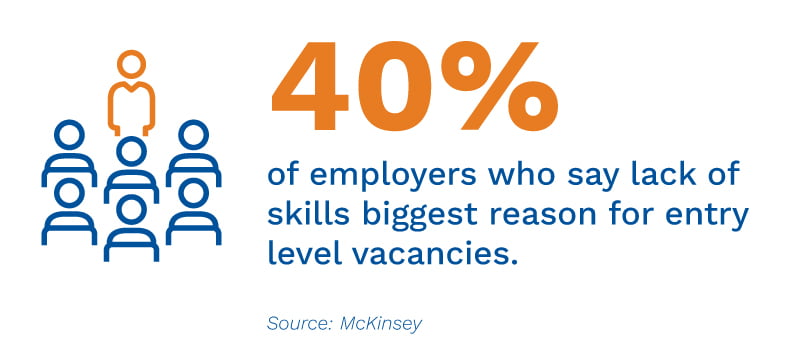

This problem is further exacerbated by the extraordinarily high number of new university graduates who are not ready for the world of work – according to McKinsey, 60% of employers say that freshly minted graduates leave college with inadequate preparation for a commercial career.

Unfortunately, employers hoping the worker supply/demand imbalance will change as financial pressures drive the estimated half a million UK workers sitting on the side-lines back to work, are also set to be disappointed.

Stubbornly high energy prices, rising corporation taxes and business rates, plus a shrinking GDP and hard-pressed consumers in bunker-mode is already impacting business incomes, limiting their ability to match employee compensation demands as returning workers want more money to re-enter the workforce. A vicious economic circle, where businesses want workers, workers are available, but businesses cannot afford to offer the wages they demand, remains a high possibility.

The UK employment outlook, where high hiring intentions must overcome acute talent shortages, is likely to be even more intense within finance and accounting roles in 2023, as all five major industries for finance and accounting skills – BFSI, IT/Tech, Manufacturing, Pharma, Retailing – report increasing demand for finance talent, and virtually all industries are seeking workers to fill the same roles and bring the same skill sets.

According to a recent Gartner survey, business leaders and HR executives should expect extreme competition for Financial Managers, Compliance Officers, and Finance Analysts throughout 2023. Accordingly, organisations should consider hiring talent for these roles outside their industries, differentiating their Employer Value Proposition (EVP) across industry players to attract candidates, and adjusting compensation packages to align with the severe imbalance of talent to demand.

And the same skills:

Source: Gartner Q4 2022

Whilst salary demands receded during the pandemic, with WFH and hybrid working becoming the top employee needs, the extreme increases in the cost of living have caused salaries to become a priority again for many accountancy and finance professionals. While some large employers have taken a positive stance to offset the cost of living by increasing salaries and offering first-class compensation packages, the UK’s economic difficulties have left many smaller businesses struggling to follow suit.

Analysis from end of 2022 reveals that 26% of UK finance and accounting workers are unhappy with their current salary and almost 30% receive no added benefits at all.

These are workers for whom the grass is always greener and will be seen as prime targets for competitors seeking to poach top finance talent.

Faced with the prospect of too few new workers to hire, and an exodus of unhappy workers they already employ, business and HR leaders must take appropriate steps to counter misgivings by candidates and current staff. Salary adjustments to counter cost of living spikes are not the only option. Employers should review their entire benefits package – including hybrid working, personal development programmes, and skills training, to avoid a labour squeeze.

High demand for digital talent is also increasing the costs of hiring at the same time as a lack of digitally-fluent workers is resulting in delayed projects and impacting companies as they fall behind their competitors.

According to a report using data from PwC and Lloyds Banking Group, more than a third of the UK’s ‘digitally literate’ workforce were unable to complete at least one of the Lloyds’ Essential Digital Skills for Work. This disturbing statistic falls against findings in the Q1 2023 Manpower Employment Outlook Survey which highlight that digital roles continue to drive UK job demand - IT businesses remain net positive at 34%, with Banking, Finance, Insurance and Real estate not so far behind – and global research indicating that 39% of employees say they’re not getting sufficient technology training from their employers to help keep their digital skills up to date.

It’s not just the commercial world that is facing these challenges. The 2022 UK civil service digital skills report revealed that the need for digital skills is a major challenge in modernising Whitehall infrastructure, with 50% of managers citing an inability to hire the digitally skilled talent they need.

39% of employees said they're concerned about not getting sufficient technology training from their employees to help keep skills up to date

A digital skills gap as large as 33% of the UK workforce indicates a severe shortage of potential workers to fulfil modern finance roles. This situation will only intensify as the influence of technology on business increases, especially in areas of finance.

In the near-term, businesses will have little choice but to pay higher salaries and be more generous with their benefits packages to secure the digitally-skilled finance talent they need. In the mid-term, and in a bid to offset a widespread digital skills shortage that will be unable to match future growth and technological ingress, organisations should invest in digital training and reskilling programmes to bring workers up to speed and to create a new finance workforce from within.

Source: Gartner

Finance employee attitudes to work have changed and their expectations have grown to encompass a range of needs, some of which are deal breakers in any hiring situation. So, while a competitive wage is the primary goal for taking a new job, or deciding to remain where they are, other job benefits are increasingly factored into employee decision-making when it comes to whom they wish to work for.

The fact is, workers want to thrive at work, not just survive. Flexible working, greater opportunity for advancement, greater recognition of worker input, upskilling, and increased wellbeing, both emotional and physical, are now firmly front and centre when it comes to employee priorities.

Source: Manpower ‘What Workers Want’

Annual and automatic salary increments

Performance bonuses

Elevated employer company pension contributions

Private healthcare

Health insurance

Workers who feel they are not receiving a package that matches their worth may vote with their feet if they do not get what they want - as evidenced by the great resignations, reshuffles, and reprioritisations of the past two years. Salaries, working environment, and company culture have different levels of importance to different cohorts of finance workers and especially to different generations.

Although there will be a continuing need to customise compensation offers based on individual skills and experience, businesses should review their general compensation bands and Employee Value Proposition (EVP) to match the expectations of both new candidates and current finance talent improving hiring success and improving staff attrition.